Record Home Prices + 7% Mortgage Rates = Market Reality Check

Why US home prices keep rising despite affordability woes, regional trends, high mortgage rates, and low supply. Trump’s tax cut proposal, the Fed’s role, Practical advice for buyers, sellers, and investors navigating today’s market.

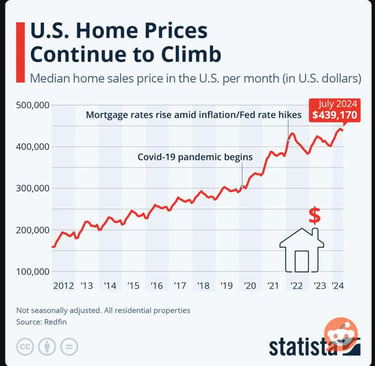

If you've been scratching your brain wondering why home prices keep climbing when everyone has predicted a crash, let's talk logistics. Home prices hitting new record highs in June. While those alarming headlines about falling sales might have you worried, the reality is more nuanced and understanding what's really happening is pretty important if you're thinking about buying or selling in today's market.

---------------------------------------------------------------------------------------------------------------------------------------

Contrary to widespread expectations of a housing market collapse, national home prices have actually increased by 1% year-over-year as of June. However, this national average masks the regional variations that tell a more complex story.

According to recent data from a leading mortgage technology firm (ICE), home prices are declining in approximately 1/3 of the United States. This means that in 2/3 of the country, prices are either holding steady or continuing to climb. The split is particularly notable: Florida and Texas are experiencing more significant price drops, while the Northeast and Midwest continue to see price appreciation. (People are moving back home)

This regional split explains why you might feel like the statistics don't match your reality. If home prices in your neighborhood have dropped 7%, that's real and frustrating but it's balanced by an 8% increase somewhere else, keeping the national average relatively stable. It's one of those situations where everyone's experience feels different, yet the data tells the broader story.

Market Activity vs. Price Movement

Recent headlines reporting "Home Sales Fall to 9-Month Low" have caused confusion among market watchers and real estate professionals. It's importatn that we distinguish between sales volume and pricing trends.

Lower sales activity doesn't necessarily mean falling prices and this trips up a lot of people. It's actually reflecting what happens when affordability becomes a real problem. Think about this: when home prices hit record highs and mortgage rates are knocking on 7%'s door, fewer people can actually qualify for a purchase.

This creates a cycle where more potential buyers are stuck on the sidelines, watching from the bench because they simply can't afford to play (for what they want anyway). At the same time, homes are sitting on the market longer, with current inventory at 1.97 million homes—that's 7.8% higher than last year, though we're still nowhere near the pre-pandemic "normal" of 2.3-2.5 million.

Trump vs. The Federal Reserve

Housing affordability has caught the attention of politicians, with President Trump publicly calling out Federal Reserve Chair Jerome Powell for keeping interest rates elevated. Trump's argument is straightforward: the Fed is "choking the housing market" by refusing to lower rates, which theoretically would they say make mortgages cheaper and help more people afford homes. HAHAH

Eliminating Capital Gains on Home Sales

President Trump has proposed a housing tax reform: the elimination of capital gains taxes on home sales. The premise is simple by removing the so-called “tax penalty,” more homeowners might feel comfortable selling, potentially easing the current supply crunch in the housing market. Today, sellers can exclude up to $250,000 in profit ($500,000 for married couples), but parabolic home values have made those limits less effective, especially in high cost regions. The NAR estimates that over 29 million single filers and 8 million married couples would benefit under this proposal.

So, who really benefits?

Under current tax law, investors get the short end of the stick. They don’t qualify for the capital gains exclusion unless they’ve used the property as a primary residence. That means landlords, flippers, and owners of second homes pay taxes on their entire profit when they sell. If this proposal becomes law, it would eliminate the need for 1031 exchanges, allow more profitable short term flipping, and reduce holding periods purely based on tax avoidance. In short, it would unleash a wave of investor driven selling and buying.

Here’s a counterintuitive take: Removing capital gains taxes could flood the housing market.. not just with primary homes, but with investor owned inventory that’s been sitting idle or rented out.

This wave of renovated, flipped properties could inject much needed supply into tight markets. But more supply means what? Potential price softening.

So ironically, a policy meant to benefit homeowners and real estate investors could potentially lead to a cooling of prices especially in overheated markets where inventory has been artificially low. That might actually be good for affordability even if it causes some short term whiplash.

Interest Rates

Current 30-year mortgage rates sit at approximately 6.8%, near the upper end of their recent range. Forecasts for the remainder of 2025 suggest modest relief at best, with rates potentially dropping to around 6.6% by the end of September.

However, predictions vary significantly among industry experts. NAR projects rates could fall to 6.4%, while the Mortgage Bankers Association expects rates to remain near current levels at 6.8%.

It's crucial to understand that the Fed doesn't directly control mortgage rates. The Fed has more influence over short term rates, while mortgage rates are more closely tied to long term bond yields. Even if the Fed cuts rates, mortgage rates might not follow proportionally.

With Jerome Powell's term ending in spring 2026, significant policy changes are unlikely until Trump can appoint a new Fed chair. This suggests that meaningful mortgage rate relief may not arrive until 2026 at the earliest.

For the remainder of 2025, expect mortgage rates to remain relatively stable in their current range. The market has been "rangebound" for an extended period, and dramatic changes appear unlikely in the near term.

Additional Considerations

Construction Costs Are Still Sky-High: Even if we see more existing homes hit the market, building new ones remains expensive. Labor shortages, material costs, and regulatory hurdles mean that new construction isn't going to rescue us from the supply crunch anytime soon. This puts a floor under prices that policy changes alone can't break through.

Millennials: Here's something that gets overlooked Millennials are still in their prime home buying years. That's a massive generation that's not going anywhere, and they're forming households and wanting to own homes. This creates persistent underlying demand that can absorb quite a bit of new inventory before prices really start to budge.

The Global Factor: Immigration patterns, foreign investment, and international economic conditions all play a role in local housing markets, especially in gateway cities. These forces operate independently of domestic policy and can either amplify or offset whatever happens with tax changes and interest rates.

The point is, even if Trump's tax proposal does flood the market with investor properties, and even if rates do come down, the housing market has a lot of moving parts. Some of them work in favor of affordability, others don't.

For Buyers, Sellers & Investors

For Buyers: The current environment requires patience and realistic expectations. While waiting for rate relief is tempting, timing the market perfectly is nearly impossible. Focus on your personal financial readiness rather than trying to predict rate movements.

For Sellers: Current conditions present some challenges and potential opportunities pending location. While transaction volume is lower, well priced homes in desirable areas continue to sell. The proposed tax changes, if enacted, could provide additional selling incentives.

For Investors: Regional market variations create opportunities for those who can identify undervalued areas. The disparity between markets suggests that local knowledge and expertise are more valuable than ever.

What's next?

The housing market isn't crashing it's adjusting to new realities of higher prices and elevated financing costs. While political pressure for policy solutions continues to build, meaningful relief likely won't arrive until 2026 at the earliest.

Success in this market requires understanding local conditions, maintaining realistic expectations, and making decisions based on personal circumstances rather than waiting for perfect market conditions that may never materialize.

Politics and housing policy add another layer of complexity, but the fundamental drivers of supply, demand, and affordability will ultimately determine market direction. Stay informed, work with knowledgeable professionals, and focus on long-term housing goals rather than short-term market timing.

Rando